Cold storage: heating up or cooling off?

Contact

Sep 6, 2022

Cold storage: heating up or cooling off?

Vanessa Rader, Head of Research for Ray White Commercial says these specialised assets will be one to continue to watch in the short to medium term particularly due to their expanded need across both food and beverage, and health science industries.

The cold storage asset class has gone through a few periods of change over the last ten years. The evolution of this industrial asset class has seen investment demand increase more recently, notably from offshore and institutional groups. Popularity in the asset was reignited again during the pandemic period with expanded use into health sciences, as the need to manufacture, store and transport various medical grade products grew. This narrow subset of an already lucrative industrial asset saw demand to purchase increase, resulting in strong compression of yields last year, albeit into 2022 this has moderated.

Growing in popularity as an asset class during the 2015-2018 period, this asset type, which was often termed as “food & beverage”, is a subsector to industrial also known as refrigerated warehousing. During this time, this sector evolved into a dynamic and less owner-occupied asset due to users demanding better innovations in technology and the changing requirements of the end consumer wanting reduced timeframes for the delivery of perishable food items. The peak in transactions was witnessed in 2014/2015 where over $450 million changed hands driven by portfolio transitions across the country, notably the eastern seaboard.

Post this period we did see tempered investment activity; however, since 2019, transactions once again grew fuelled by quality stock being completed, together with the increasing retail demand for fresh food, as well as quickly changing health science needs. During the 2021 calendar year over $320 million has changed hands with yields ranging from as low as 4.3 per cent through to 5.5 per cent, with institutional demand instrumental in compressing these yields which were in the 6 per cent to 7.5 per cent range a few years prior. During 2022, however, transaction levels have decreased inline with the overall decline in commercial investment activity, due to rising interest rates and inflation which is expected to impact yield levels.

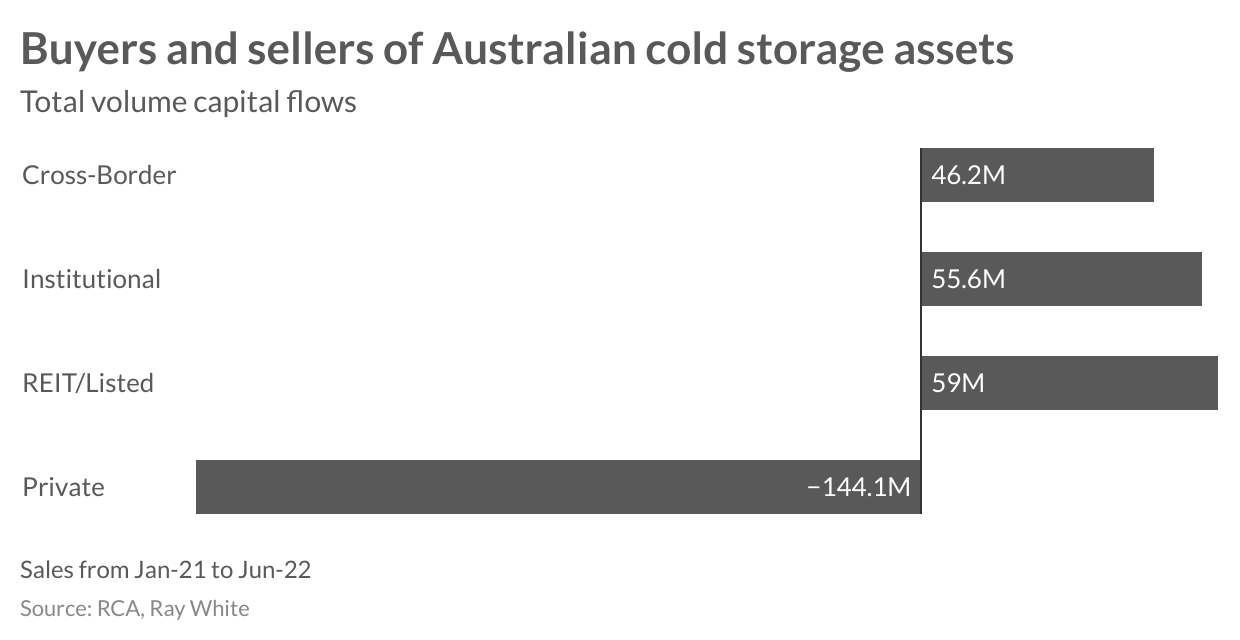

Refrigerated facilities that cater to food and beverage production, along with refrigerated warehouse and distribution facilities in Australia attracted several new players over the past five years, notably international companies with strong track records in their own respective countries. Since this time, we saw ongoing interest from these offshore buyers and domestic institutional investors fuelling competition for this bespoke asset type. Looking at sales over the past 18 months, the continued decline in owner-occupiers is clear, representing more seller activity while a combination of cross-border, institutional and REITs as net buyers seek to capitalise on high user demand, low vacancy and rising rental rates in the current high inflationary market.

Looking ahead, despite high occupancy and ongoing need for cold storage assets, broader market conditions will see some moderation to yields and slow down in investment activity; however, these specialised assets will be one to continue to watch in the short to medium term particularly due to their expanded need across both food and beverage, and health science industries.

Important Information:

Contact details:

Vanessa Rader

RWC

0432 652 115

Email

17739

17478

Vanessa Rader