The resurgence of student accommodation in Australia

Contact

Feb 7, 2023

The resurgence of student accommodation in Australia

According to Vanessa Rader, Head of Research for Ray White Commercial, while student visa numbers are down more than 50 per cent, enrolment levels have seen a strong increase during late 2022 particularly from India. Coupled with the changing legislation in China, it is expected that student enrolments could eclipse 2019 levels during 2023/204.

-

Vanessa Rader, Head of Research for Ray White Commercial.

Vanessa Rader, Head of Research for Ray White Commercial. -

-

The student accommodation sector continued to be active during the COVID-19 period despite the closure of borders and the move to online learning. Major international players such as Scape and GIC continued to purchase portfolios of assets across the country highlighting their long term confidence in the sector. However, once in-person study resumed we continued to see low international enrolments. Instead, operators capitalised on low residential vacancy rates which saw domestic students grow their occupancy levels. Discouraging, however, has been the international student visa numbers in 2022, raising concern that remote learning could be here to stay as a viable alternative for many overseas students, impacting this sector going forward.

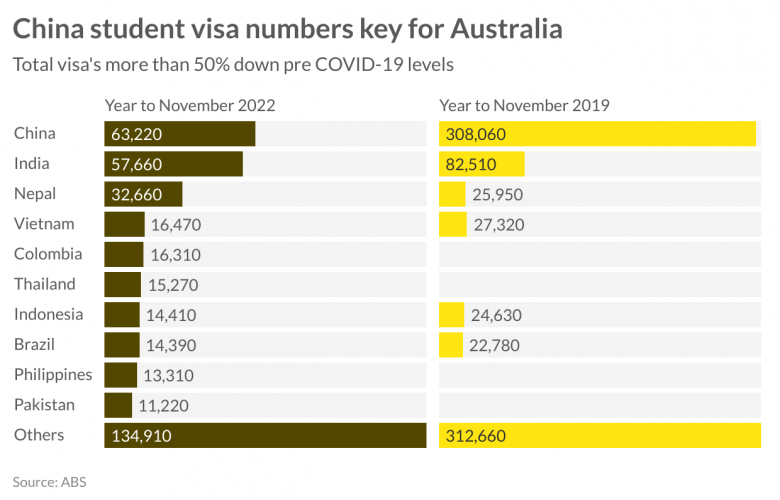

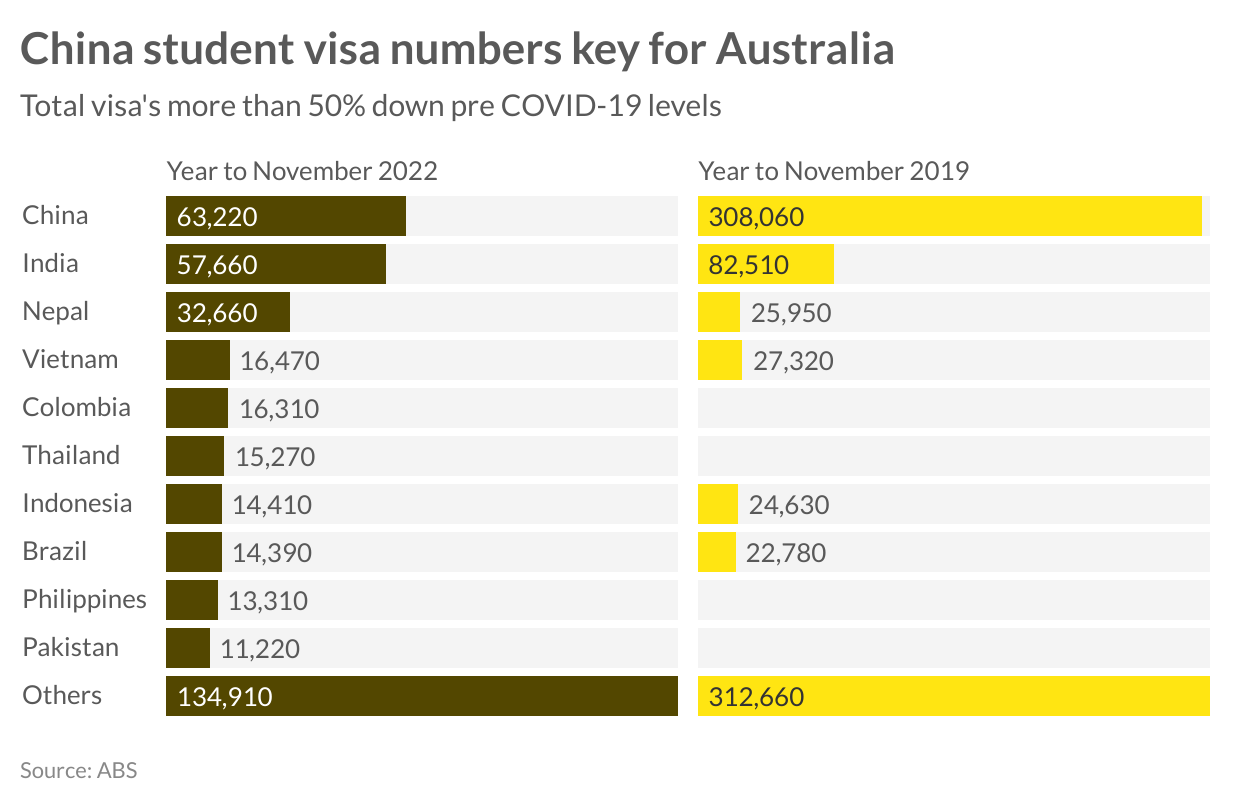

While there was some uptick in visa numbers in late 2022, we have seen that total students are still more than 50 per cent down pre COVID-19 levels. Annual data to November highlights this decline, with the large majority of this fall due to the Chinese student population. However, encouragingly, there has been an increase in other locations such as Colombia, Thailand, Philippines and Pakistan. Political and economic uncertainty was expected to keep these numbers low over the short term despite borders opening and classroom learning resuming. An announcement has recently been made that China has changed their policy, which was in place during the pandemic, which allowed for online courses from foreign universities to be delivered to students within China. This is set to see a rapid increase in Chinese students crossing the border ready for the 2023 learning year.

With Australia one of the major beneficiaries of these students, the visa numbers are expected to revert quickly back to levels seen prior to COVID-19, which brings along issues of accommodation. With residential vacancy rates at historic lows across the country and occupancy within purpose built student accommodation facilities already high, the expected need for additional accommodation options will grow quickly. There are currently eight major projects under construction across the east coast, representing approximately 2,500 rooms. Despite the high cost of construction, the strong increases in rates achieved during this mismatch in supply has improved the viability of these new developments.

While student visa numbers are down more than 50 per cent, enrolments represent a 21.8 per cent decline in the year to November 2022 compared to November 2019. Enrolment levels have seen a strong increase during late 2022 particularly from India. Coupled with the changing legislation in China, it is expected that student enrolments could eclipse 2019 levels during 2023/204.

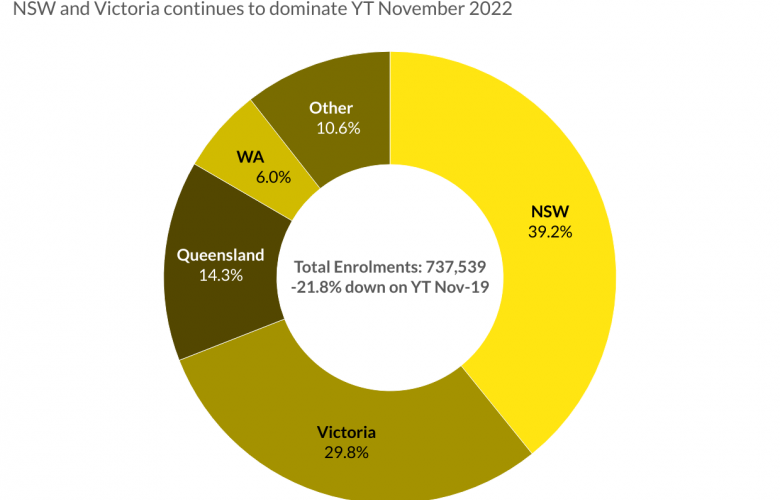

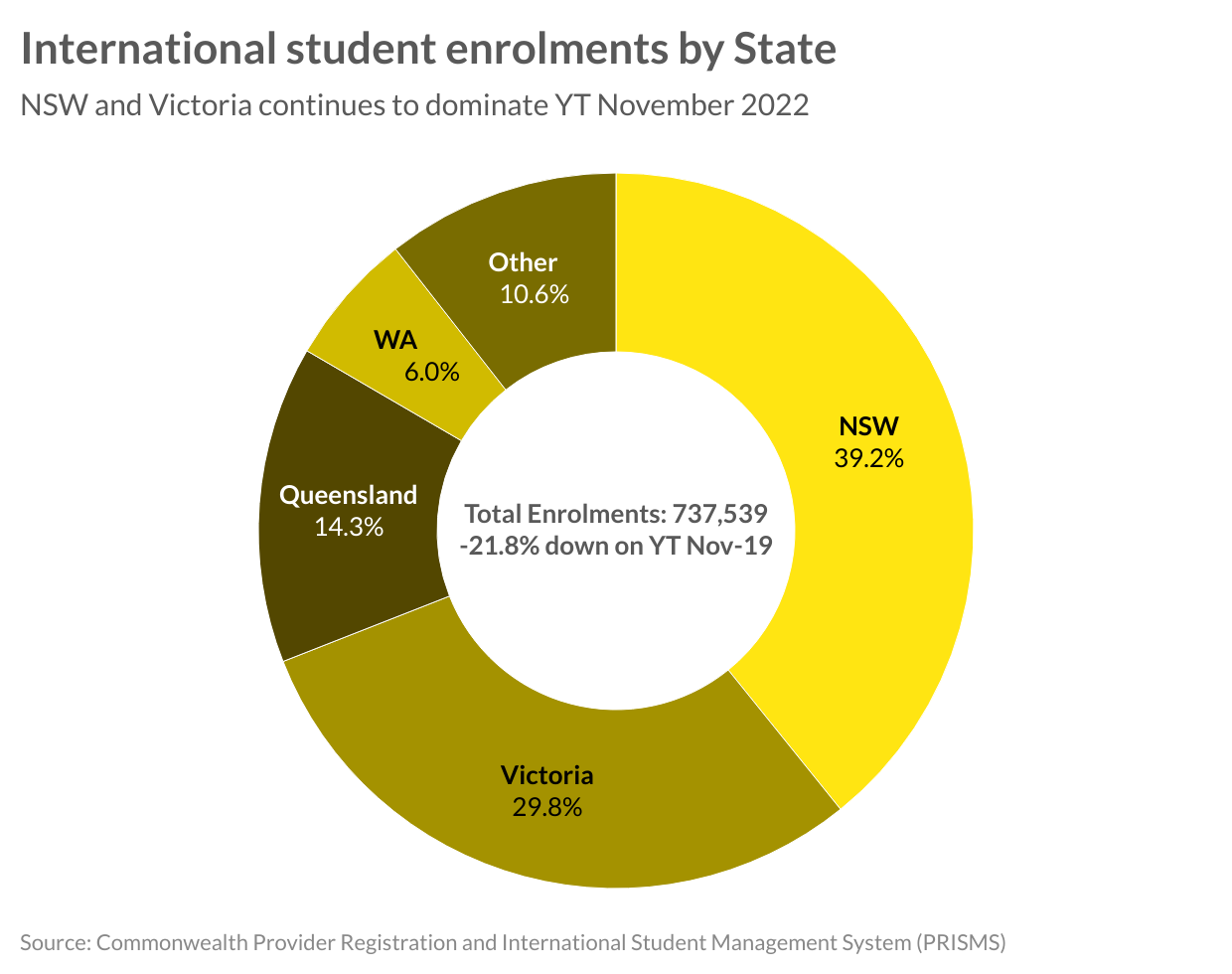

This rapid growth in numbers will continue to pressure the student accommodation sector with NSW, Victoria, Queensland and WA anticipated to be the main contributor to new enrolments and the main beneficiary of new supply projects, while enrolment numbers have already reached pre COVID-19 levels in SA, Tasmania, NT and ACT.

Important Information:

Contact details:

Vanessa Rader

RWC

0432 652 115

Email

17924

17478

Vanessa Rader