HOME >

SELECT LOCATION

What are commercial investors buying this year?

Contact

Apr 4, 2023

What are commercial investors buying this year?

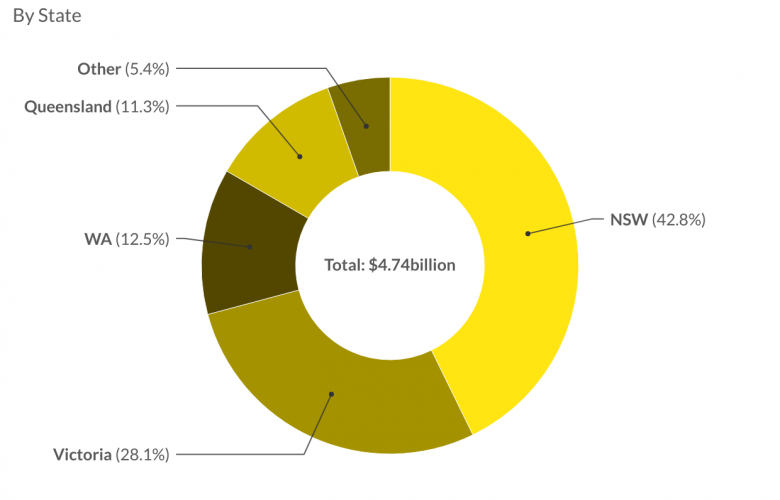

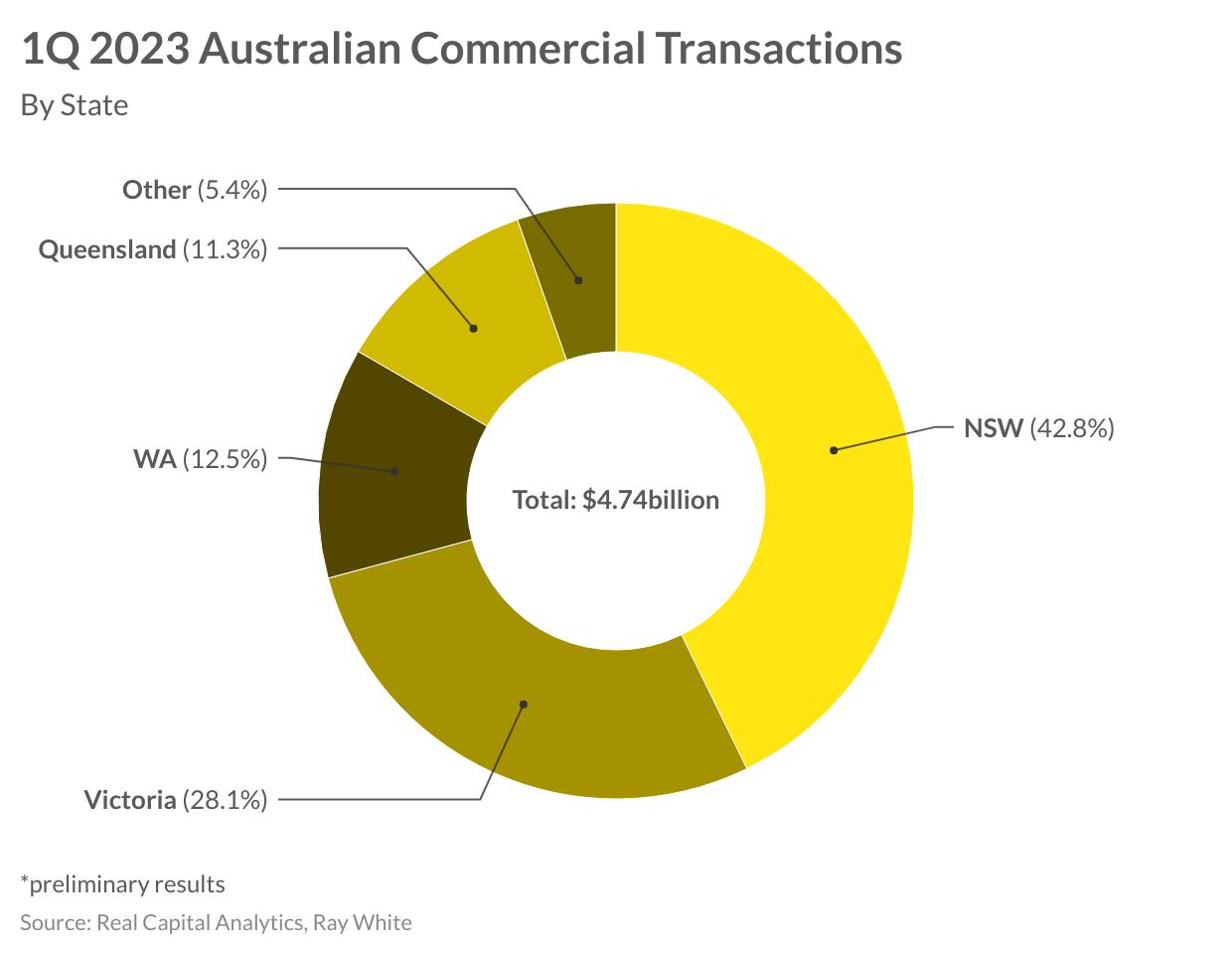

NSW remains the key market for transactional volumes, helped along by a number of high value asset transactions, notably in the retail and hotel sectors. Nationally preliminary sales volumes for the first quarter of 2023 have hit $4.74 billion down 68.2 per cent on the same time last year where sales approached $15 billion says Vanessa Rader Head of research Ray White Commercial.

NSW remains the key market for transactional volumes, helped along by a number of high value asset transactions, notably in the retail and hotel sectors. This year 42.8 per cent of sales were across NSW, similar to the 44 per cent recorded in the same time period of 2022. Victoria is the second most popular market to invest in, growing its appeal to represent 28.1 per cent, up from 22.2 per cent last year.

The largest market mover this year has been Western Australia, now the third most popular state to invest in. We have seen a number of local, interstate and international buyers look to Western Australia and its economic strength and affordable price point as a market to speculate in. While Western Australia has recorded a major retail transaction propping up these numbers, strong population gains have resulted in improvements in occupancy for office and industrial assets, while an uptick in tourism has also seen hotel and retail assets grow in popularity with the expectation of future income return movements. This year we have seen Queensland’s investment dwindle to now represent just 11.3 per cent of sales, after growing to 20.2 per cent last year, despite their strong population push.

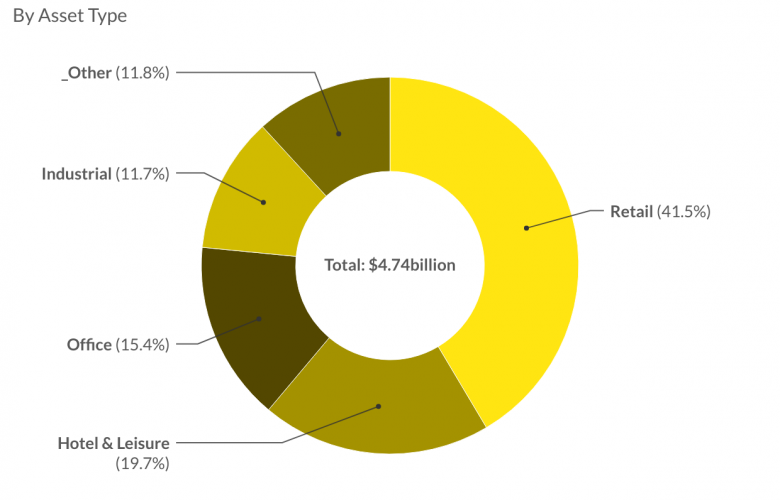

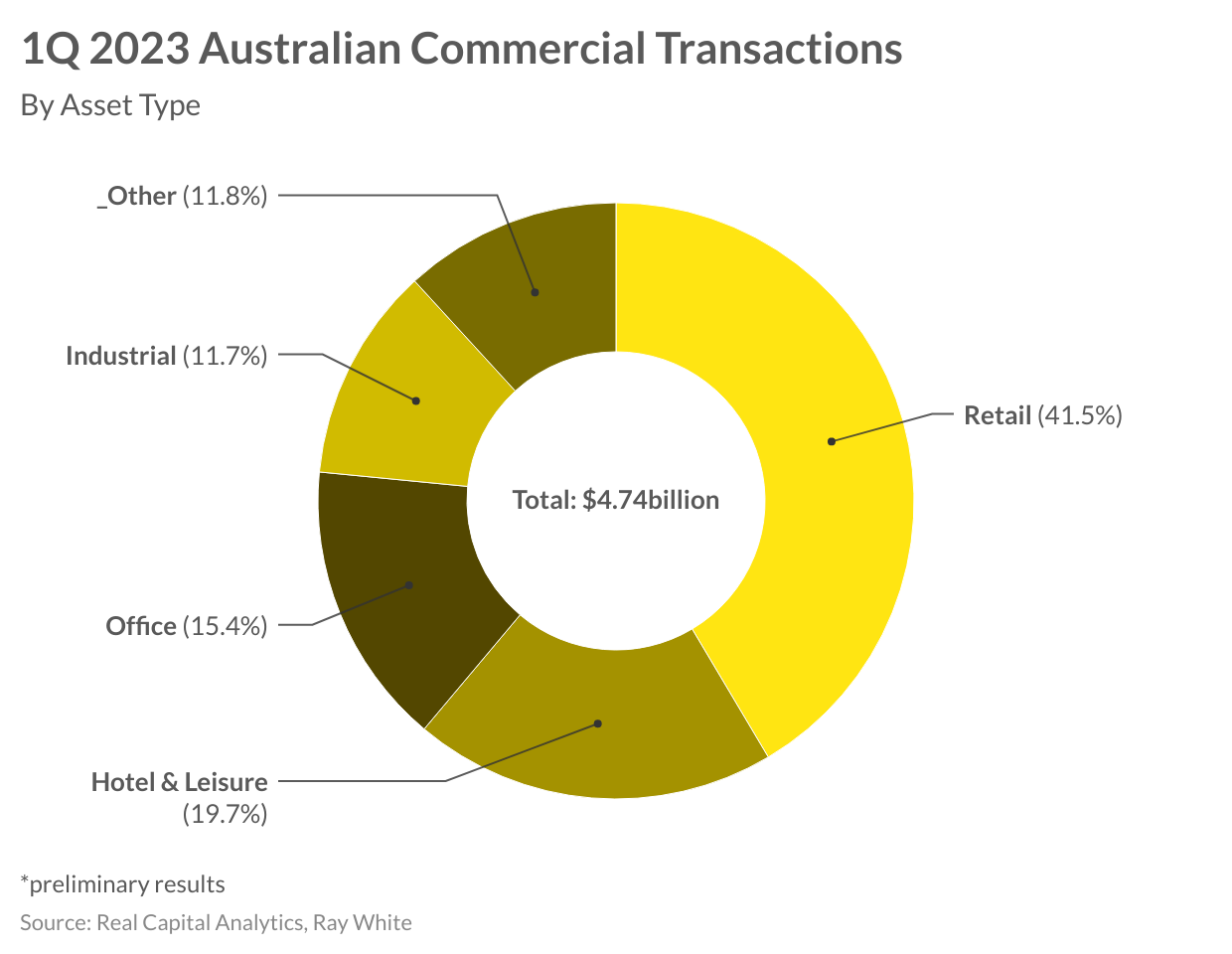

By asset class this year we have seen retail take poll position due to a number of larger sales such as Rockingham Shopping Centre in Western Australia, Craigieburn Central and Forest Hill Chase in Victoria, and Menai Marketplace and Stanhope Village in NSW.

HomeCo acquires $242.5m in shopping centres from LendLease - CBRE and JLL

The appetite for investors to purchase these sub-regional sized centres highlights the changing retail trade trends surrounding the growth in food, convenience and attractiveness of discount department stores such as K-mart. During the first quarter of 2023 nearly $2 billion in retail sales occurred, representing 41.5 per cent, and while the volumes remain well below Q1 2022 results, its portion is up to 27.4 per cent. Office has halved its proportion of all investment this year, there were limited larger trophy sales compared to the same time last year, resulting in this asset class accounting for just 15.42 per cent. Similarly, industrial activity has slowed particularly at the upper, institutional end, while smaller private investor and owner occupier activity continues strongly, particularly in the sub $1.5 million price range, with more than 300 transactions occurring at this price point so far this year.

Attracting the most attention in 2023 has been the hotel and tourism sector, again spurred on by a range of international branded hotel sales including Waldorf Astoria in Sydney and Sofitel in Brisbane. A number of budget chains and private offerings have also changed hands capitalising on the strong gains in average room rates and the uptick in international and domestic travel activity, this year accounting for close to 20 per cent of all sales, up from 6.4 per cent last year.

Across the alternatives sector, activity is still occurring, albeit at a much slower rate. Childcare across the country has recorded 46.3 per cent decline in sales activity compared to first quarter 2023, while service stations and medical asset volumes are down over 80 per cent compared to the same time last year. While high construction costs continue to plague the development site market, sales this year only represent 12 per cent of what was transacted the same time last year.

It's prudent to remember that the commercial property market has come off a strong two years in sales volumes, capitalising on historic low interest rates and availability of finance, while strong income gains for some asset classes also saw an increase in purchasers entering the market. As conditions have changed, we have seen many less experienced buyers leave the market, and many opportunistic investors jump. These buyers are moving with less urgency or are seeking out distressed assets or value add opportunities at the right price. As a result, we expect to see volume this year remain subdued, while REITs, funds and offshore buyers are likely to proceed with caution given the global banking turmoil which continues to unfold.

Important Information:

Contact details:

Contact details:

Vanessa Rader

Ray White Head of Research

+61432 652 115

Email

18065

8806

Vanessa Rader