HOME >

SELECT LOCATION

Shifting gear to income growth as property moves past peak uncertainty - Knight Frank

Contact

Aug 21, 2024

Shifting gear to income growth as property moves past peak uncertainty - Knight Frank

By Knight Frank Chief Economist Ben Burston.

Clouded by multiple uncertainties since early 2022, property investment has been stuck in the slow lane.

For some time, investors have been asking the same questions:

- How long would inflation persist?

- How high would interest rates rise?

- To what extent would asset values need to adjust?

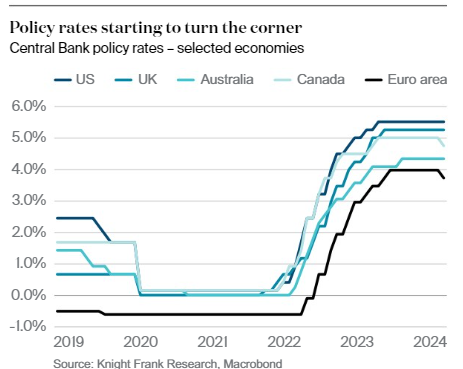

After over two years, these remain important questions, but from a global perspective the degree of urgency has been dialled down as the answers are increasingly known and where uncertainty still persists, it has fallen back within a more normal range. Inflation is subsiding, albeit after a few bumps in the road.

Interest rates have peaked in the major economies and begun to retrace in Europe and Canada. And after a substantial adjustment, capital values have stabilised and in some cases returned to growth.

Job nearly done

In Australia, progression on these key questions has been slower and attention is still focussed on sticky inflation in service industries and the related risk of further rate hikes.

However, even among the more hawkish commentators, there is recognition that most of the RBA’s work is done and that rates are more likely to be lower than at the same level or higher in 18 months’ time.

Reflecting this, sentiment in property markets is improving and prime yields have largely stabilised across all sectors, including in offices where the uncertainty and lack of liquidity has been most acute.

After only a handful of deals over the past two years, the past two months has seen a spate of large office deals in Sydney, Brisbane and Melbourne that will go a long way to establishing a new baseline for pricing and unlocking further activity.

Taken together, this means we have a clearer picture on the market’s cyclical trajectory, with much less downside risk to property values arising from the macro outlook compared to recent years.

Movement underneath the surface

For property investors, this shifts the focus beyond mitigating risk towards future growth potential, and the ability to drive performance through income growth in particular.

Here, there has been considerable movement underneath the surface, even while the cyclical dynamics has been centre stage.

Office rents have returned to growth, but the pattern is different to the recent past, with growth led by Brisbane and Perth, and the core precincts of Sydney and Melbourne out-performing the wider market.

In the retail sector, leasing spreads have also turned positive after a protracted period of weakness, and MAT growth in major shopping centres has picked up off the back of increasing centre visitation, notwithstanding the pressures on discretionary spending.

And in the emerging living sectors, a confluence of supply pressures, high population growth and declining household sizes are driving a rapid escalation in apartment rents that continues to attract the attention of investors and developers locally and globally.

Silver linings playbook

Though this has been occurring against the backdrop of a sluggish economy may surprise, some of the elements of that slowing economy have actually contributed to income growth.

Most obviously, the steep rise in construction costs that has been emblematic of the high inflation environment has stifled construction activity across all sectors, thereby tilting the supply-demand dynamic and contributing to rental growth.

Also, indexation for inflation in lease agreements – either directly or indirectly through higher agreed escalation clauses – has naturally helped income grow, mitigating the impact on values from the cyclical pressure of higher cap rates.

Tuning out the noise

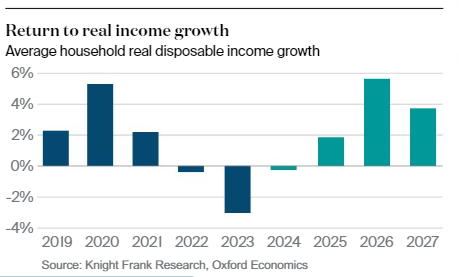

Looking ahead, the ingredients are in place for a further broadening in income growth that will support investment returns in 2025 and beyond. A return to growth in real incomes for households will be an important contributor, as rising wages, tax cuts and declining inflation take effect.

Oxford Economics forecast a strong turnaround in 2025 after a historically deep contraction, reverting back to 1.8% growth and even stronger growth of 5.4% in 2026.

On top of this, the backlog of demand arising from the population surge will continue to open up new opportunities, generating demand for more stock across multiple sectors and shifting the pattern of demand as governments respond with the roll-out of new infrastructure projects to improve connectivity and open up new markets.

Among the centrepiece initiatives are Sydney’s Metro and Western Sydney airport, Melbourne’s Metro Tunnel, Brisbane’s Cross River Rail and Perth’s Metronet.

As time goes on, the focus on these growth drivers will take over as uncertainty over the macro picture gives way to a brighter outlook. Investors looking through the noise with a clear view on how to position themselves for income growth will be best placed to out-perform as the market shifts firstly to recovery and then on to the next growth cycle.

For more insights into Australia’s Capital Markets, download Knight Frank’s Capital Exclusive report: Capital Exclusive 2024 (knightfrank.com.au)

Important Information:

Contact details:

Contact details:

Ben Burston

Knight Frank Australia Chief Economist

+61 452 661 682

Email

19219

6844

Ben Burston