HOME >

SELECT LOCATION

CBD retail vacancy rates continue to tighten across most of Australia’s major cities - CBRE

Contact

Aug 27, 2024

CBD retail vacancy rates continue to tighten across most of Australia’s major cities - CBRE

Retail vacancy rates across Australia’s capital cities remains tight with Melbourne’s CBD continuing to hold the lowest vacancy rate in the country says Head of Retail Research Kate Bailey and Head of Retail Property Management & Leasing Sheree Griff.

Retail vacancy rates across Australia’s capital cities remains tight with Melbourne’s CBD continuing to hold the lowest vacancy rate in the country.

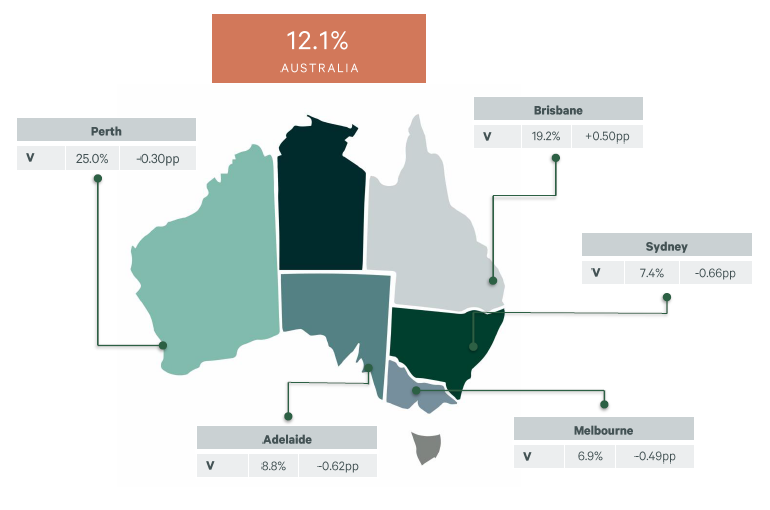

CBRE’s Australian CBD Retail Vacancy H1 2024 report found across the five surveyed capital cities, Melbourne had the lowest vacancy in the country at 6.9% with a reduction of 50bps compared to H2 2023.

The Sydney CBD recorded the largest reduction over the half, of 66bps, with a 7.4% vacancy. Both the Perth and Adelaide markets also tightened with a vacancy of 25% and 8.8% respectively. Brisbane was the only city to record an increase in vacancy of 50bps to 19.2%, however, this is still lower than the same period in 2023 (19.5% H1 23).

The report also shows Australia’s total retail CBD vacancy decreased 39bps to 12.1% in H1 2024.

CBRE’s Head of Retail Research Kate Bailey noted, “Overall, vacancy has tightened nationally. The return to office, coupled with increased tourism and international student inflows, has led to increased foot traffic in CBDs, supporting occupier appetite for floorspace within these cities.”

A total of 5,646 CBD retail outlets were surveyed for the report. Melbourne had the highest number of retail outlets surveyed at 1,720, followed by Sydney (1,553), Brisbane (1,335), Perth (673) and Adelaide (365).

CBRE’s Head of Retail Property Management & Leasing Sheree Griff said, “Retail continues to perform well, despite the cost of living pressures. More brands are focused on quality, immersive experiences in their bricks and mortar spaces which is meeting the needs of consumers who are being more purposeful with their spending.

“We expect to see leasing growth to remain steady across 2024 as retailers continue to seek ways to showcase innovation and add value to their bricks and mortar offering.”

Sydney

Sydney CBD retail vacancy has tightened during H1 by 66bps. This is the second consecutive half-yearly contraction since H1 2023, coming off a previous peak vacancy of 10.8%.

Despite overall vacancy contracting, strip retail vacancy softened this half to 8.1% (or +0.27pp).

CBRE’s Australian Head of Retail Leasing Leif Olson said demand for core strip locations in the CBD remains strong as occupiers seek to promote brand awareness and push product sales.

“Over the past six months Sydney’s core CBD continued to see a strong inflow of local and global brands securing flagship tenancies in strip locations including MJ Bale at 1 Martin Place and Rodd & Gunn at 14 Martin Place.

“With the new metro opening, we expect the improved connectivity and accessibility will drive increased pedestrian traffic to new areas of the CBD which will result in a further decline in vacancy across prime and secondary retail space.”

Arcade retail vacancy saw the largest decline in H1 (-1.20pp) to 6.9%. This is in part driven by the major refurbishment of The General Post Office which has seen an increase in leases signed, including MJ Bale’s new flagship store (240sqm).

Centre retail vacancy tighten by 0.47pp to 7.7%. The continued strong performance of luxury brands and new food and beverage entrants continue to bolster Sydney’s CBD centres, with steadily increasing foot traffic and office workers.

Melbourne

Melbourne’s CBD retail vacancy declined by 50bps. This is the second consecutive decline in retail vacancy, with the CBD reaching a new post-pandemic low.

CBRE Director of Retail Leasing Jason Orenbuch noted, “Melbourne’s CBD continues to experience a period of significant change. Developments are underway in some of CBD’s major traffic thoroughfares such as Bourke Street Mall, Collins Street, Elizabeth Street and Swanston Street, these projects will further bolster activity and activation of Melbourne’s streetscapes.

“Landlords across Melbourne continue to invest in existing assets which is fuelling improved performance. There are a number of major retail redevelopments underway and once these are completed, in 2025 and beyond, we expect tenants across the CBD will be inclined to make more proactive leasing decisions. We expect this will likely drive vacancy towards the historical average of 4%.”

Vacancy across all three retail categories (strip, shopping centre and arcade) decreased in H1 2024, with the largest recorded decline in laneways and arcades of 120bps with a vacancy rate of 12.7%.

Declines in vacancy were recorded in both strip (-10bps) and shopping centre (-40bps) locations, although at lower levels compared to previous survey periods. Significant bifurcation remains in both strip and shopping centre locations, with non-core locations showing significantly higher vacancy than core locations.

Brisbane

Brisbane CBD’s increased retail vacancy can be in part attributed to the ongoing impacts of the COVID pandemic as well as upcoming refurbishments of existing centres.

CBRE Senior Director of Retail Leasing Andrew Woodgate noted, “The Brisbane CBD has experienced a solid return to office, strong population growth and a steady improvement of international tourism which is supporting Brisbane’s retail market. Many events have also attracted visitors into Brisbane’s CBD, including multiple sold out concerts and sporting events such as the women’s soccer World Cup, NRL magic round, Wallabies test matches and State of Origin.

“The redevelopment of Post Office Square has increased demand for new food retail tenants particularly in QSR (quick service restaurants) and in H1 we saw the re-opening and opening of many hospitality retailers including Melt Brothers, Lena’s Bakehouse and Chow Chow.

“Upcoming major redevelopments are expected to further revitalise the Brisbane CBD. These include the Eagle Street Pier redevelopment, new retail space in Queen’s Wharf, and the ‘Queens Laneway’ precinct under QIC’s new headquarters at 360 Queen Street which will rejuvenate the northern end of the CBD and improve pedestrian access from the Golden Triangle to Adelaide Street.”

CBD strip led the increase in Brisbane retail vacancy, softening by 105 bps to 16.3%. A significant bifurcation remains within the CBD strip, with non-core locations recording higher vacancy compared to core locations. Demand for core locations remains prominent, particularly for clothing and emerging luxury retailers wanting to open flagship stores in prime core strip locations to remain competitive.

Retail centre vacancy in the CBD decreased marginally by 59bps to 25.3%. This decline was partly driven by well-established core super prime centres, which feature many luxury retailers and benefit from premium locations. Arcade retail vacancy remained stable this half at 15.7%.

Perth

In H1 2024, vacancy declined by 30bps to 25%. While the vacancy rate is still relatively high in Perth, it has continued to trend down and is the lowest vacancy rate recorded in the past three years. Retail vacancy in Perth’s CBD has declined by 150bps since reaching 26.5% in H1 2022.

The improvement in vacancy in H1 2024 was driven by CBD centres which declined by 75bps to 25.3% and strips which declined by 29bps to 23.9%. Vacancy in arcades increased slightly by 7bps to 27.7%.

The core retail strip of the Murray Street Mall and Murray Street, which is transforming into a high-end luxury shopping precinct, is predominantly driving the vacancy improvement in CBD strips.

CBRE Senior Director & WA Head of Retail Fred Clohessy said, “The transformation west of the Murray Street Mall into a luxury retail precinct continues, with Gucci relocating from King Street and Dior, Omega, Cartier and Longines (on the corner of the Murray Street Mall) expected to open stores soon.

“Overall, the Perth retail market faces ongoing national headwinds including inflationary pressures, restrictive interest rates, and moderating economic conditions but this is counterbalanced by continuing tailwinds including WA’s nation leading population growth, economic and tourism growth, Perth CBD’s nation-leading office occupancy rates and fiscal stimulus provided by Federal and State governments.

“Longer term, the development of ECU’s Perth CBD campus is a watershed project for the Perth CBD and the retail market. The campus is expected to reach completion in late 2025 with students expected in semester one 2026. ECU’s Perth CBD campus is expected to significantly further boost activity and population growth in the Perth CBD and increase retail spending.”

Adelaide

Adelaide CBD’s retail vacancy continued to improve in H1 2024, declining by 74bps to 8.8%. This is the third lowest vacancy rate of all the major CBD markets around Australia, behind Sydney and Melbourne.

CBRE Director of Retail, Julia Pottenger said, “Retail vacancy in the Adelaide CBD has been on a positive downtrend over the past few years driven by solid economic growth post-pandemic and strong population growth, which has buoyed the overall retail markets and supported consumer spending.

“Adelaide CBD has strong visitation trends which is supporting the improving retail market. Among the notable new openings in the CBD are stationery brand Milligram’s first South Australian store in Rundle Mall and fashion brand Cable opened on Rundle Street.”

The decline in retail vacancy during H1 2024 was driven primarily by improvements across the Adelaide CBD retail strips and centres with vacancy in the arcades remaining stable.

Within the CBD centres including Rundle Place and Myer Centre, H1 2024 vacancy improved by 71bps to 11.1%.

After undergoing significant transformation over the past year with the addition of an entertainment precinct on the top floor occupied by Funlab, Rundle Place has become the main contributor to the improved vacancy rate observed in the CBD centres.

Within the CBD retail strips, H1 2024 vacancy along the core Rundle Mall retail strip improved by 69bps to 8.3% and the Adelaide Arcade continued to perform strongly with vacancy remaining stable at 2.0%.

Important Information:

Contact details:

Contact details:

Kate Bailey

Head Retail Research CBRE Australia

+61 3 8621 3411

Email

19232

12542

Kate Bailey

Jason Orenbuch

CBRE - Senior Manager Retail Services

+61 418 310 693

Email

19232

15510

Jason Orenbuch

Julia Pottenger

CBRE - Associate Director - Retail, Australia

+61 409 019 366

Email

19232

17689

Julia Pottenger

Leif Olson

CBRE Director of Retail Leasing

+61 409 748 136

Email

19232

12822

Leif Olson

Fred Clohessy

CBRE Senior Director & WA Head of Retail

+61 408 094 978

Email

19232

17690

Fred Clohessy

Sheree Griff

CBRE

Email

19232

19233

Sheree Griff