HOME >

SELECT LOCATION

New equilibrium for retail investment in Australia - JLL

Contact

Sep 5, 2024

New equilibrium for retail investment in Australia - JLL

JLL’s flagship “All-in on retail” event showed why sentiment towards the sector has turned and investors are now optimistic about the outlook.

Global real estate service firm, JLL has pointed to a number of themes illustrating how retail assets are showing a strong returns outlook, drawing attention from institutional investors who are returning to the sector.

JLL Research presented at a Retail Outlook event in Sydney shows:

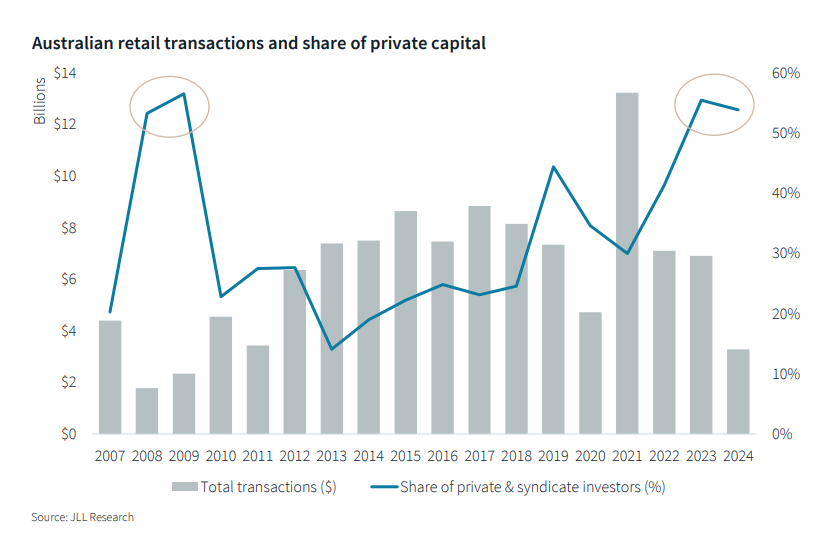

- Private investors and syndicates have been the most dominant players in the retail sector in Australia – accounting for the highest share of transactions since the GFC;

- Institutional investors, who moved away from retail before the pandemic, are re-weighting back into the sector;

- Retail investment fundamentals have reached a new equilibrium – retail rents have rebased after dipping throughout the pandemic; retail values have stabilised and the retail returns outlook has improved materially;

- Retail asset replacement costs are high, which will keep supply low and support rental growth;

- Globally, the buyer profile for retail has been diverse, with some major players returning.

JLL’s Head of Capital Markets Research – Australia, Andrew Quillfeldt said there’s a number of indicators pointing to a new equilibrium for retail, despite the liquidity headwinds which remain.

“Retail has now reset in terms of the investment fundamentals. We can see that clearly in key investment metrics, which are all supportive of a strong return outlook for the sector.”

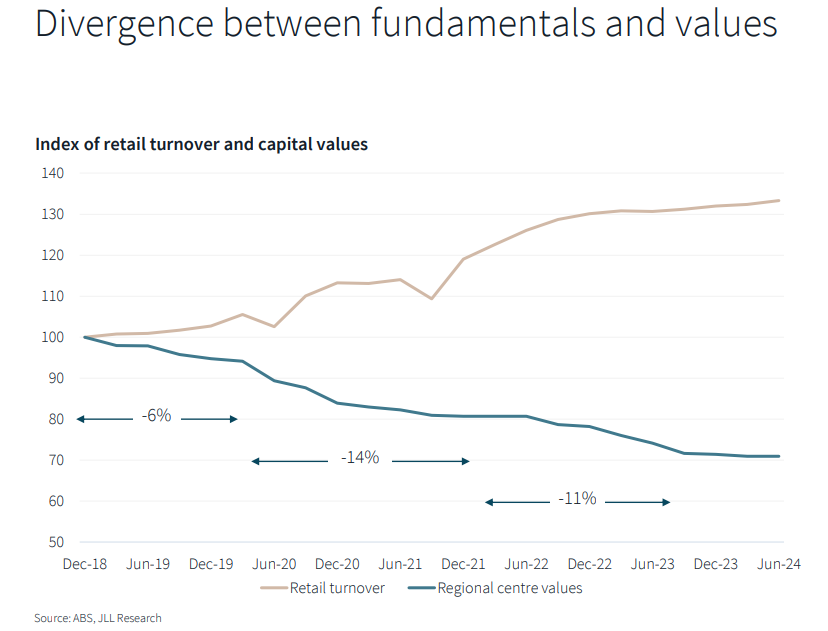

JLL’s Research outlined three phases on the decline in asset values - using larger Regional shopping centres as an example.

- The pre-pandemic phase from 2018 to early 2020 - As cap rates expanded on concerns over income sustainability, this contributed to a 6% decline;

- The COVID impact between early 2020 to Q1 2022 – This phase saw values decline 14%, which was largely driven by income rebasing (lower);

- Q1 2022 and Q3 2023 - 11% decrease in values as the risk-free rate (10-year Australian Government Bond Rate) began to increase significantly.

“The outlook for returns on retail investments is more compelling than it has been in quite a long time. We expect strong population growth, along with the current undersupply of retail floorspace, will be a major driver of sales productivity and rental growth over the next five years,” said Mr Quillfeldt.

Australia's retail sector is facing record-low new supply, with the development pipeline for 2024 and 2025 representing only 21% of the 10-year average.

“Australia’s population will grow by 1.7 million people over the next four years, and historically 1 sqm of retail has been built for every extra person, implying a need for up to 1.7 million sqm. However, there is currently only 521,000 square metres completed or under construction and due to come online over the next four years (2024-2027 inclusive),” said Mr Quillfeldt.

JLL’s Head of Retail Investments – Australia, Sam Hatcher said: “There is a growing recognition of value in retail which is encouraging investors back to the sector. JLL’s analysis shows a big divergence between retail turnover which has grown by over 30% while asset values have fallen by 30%, so there is a deep value gap. With a looming supply shortage forecast, particularly for Regional and Sub-Regional shopping centre assets, this feeds into the investment case. Our analysis also shows assets are trading at a material discount to replacement cost at around 40% which provides a long runway for rental growth.”

Australian retail accounts for the highest share of transactions across major real estate markets:

On the world stage, JLL analysis shows retail is a deeper and more active sector in Australia.

JLL Senior Director, Retail Investments – Australia, Nick Willis said: “Australia recorded the highest share of retail direct investment volumes across eight country markets over a period of 2018 to the second quarter of 2024. Retail’s percentage share of Australian transactions was 24%, followed by China at 18%, Germany at 14% and France, UK and Japan at 13%.

“Retail transactions are increasing globally, with retail and hotels the only two sectors globally to record an increase in transaction activity in 1H24 versus 1H23. We’re seeing a diverse range of buyers for retail globally and some of the big names are re-entering the sector.

“We have seen private investors play a dominant role in the sector in Australia, while institutional capital is returning to position for the next phase of the cycle. Consumer resilience has really helped improve the fundamentals for retail property,” said Mr Willis.

Private capital has been dominant in Australia, accounting for >50% of transactions:

Mr Willis said: “Private capital has been filling the capital void left by institutional divestments over the last few years, having acquired over $12.5 billion since 2020. The last time private and syndicate investors were this active in the retail sector was post GFC when counter cyclical purchases were made. The private investor and syndicate participation peaked in 2009 at 57% and this year we’re already nearing that peak at 54%.”

Important Information:

Contact details:

Contact details:

Andrew Quillfeldt

JLL

+61 2 9220 8728

Email

19265

7192

Andrew Quillfeldt

Sam Hatcher

Head of JLL Retail Investments Australia & New Zealand

+61 409 899 691

Email

19265

12362

Sam Hatcher

Nick Willis

Senior Director of JLL Retail Investments Australia & New Zealand

+61 409 595 803

Email

19265

12402

Nick Willis